Options for settings of the X13 method

This section discusses the options available for the X-13ARIMA-SEATS specifications, which are based on the original X-13ARIMA-SEATS program developed by the U.S. Census Bureau. The X-13ARIMA-SEATS specifications are – to a very large extent – organised according to the different individual specifications of the original program and are presented in the order in which they are displayed in the graphical interface of JDemetra+.

A list of the X-13ARIMA-SEATS specification’s sections

To avoid unnecessary repetitions, click on the respective link for a description of the following sections of the TRAMO/SEATS specification:

This section focuses on the decomposition part of the seasonal adjustment process and the benchmarking options.

To facilitate the comparison between JDemetra+ specifications and specifications used in Win X-13, under each option the name of the corresponding specification and the argument from the original software is given, if any. For an exact description of the different parameters, the user should refer to the documentation of the original X-13ARIMA-SEATS program. For each parameter the default parameter value, which is displayed for a template created in the Workspace window, is reported (in the Workspace window go to the Seasonal Adjustment section, right click on the x13 item in the specifications node and select New from the local menu).

For the pre-defined specifications the items are fixed, while in the case of the user-defined specification the user can set them individually. However, in some cases the choice of a given value results in a limitation of the possible alternatives for other parameters. Therefore, the user is not entirely free to set the parameters values.

Series

In the context of seasonal adjustment it is usually assumed that long time series are those exceeding twenty years of length. Performing seasonal adjustment of long time series can be difficult. Over such a long period the underlying data generating process can change, determining changes also in the components and in the components structure. In this case the adjustment over the whole series may produce sub-optimal results mainly in the most recent period and in the initial parts of the series. Therefore it is reasonable to limit long time series to the most recent observations. The Series section allows the user to limit the span (data interval) of the data to modelled or seasonally adjusted.

Series span → type

–; –

Specifies the span (data interval) of the time series to be used in the seasonal adjustment process. When the user limits the original time series to a given span, only this span will be used in the computations. The available parameters for this option are:

- All – full time series span is considered in the seasonal adjustment;

- From – date of the first time series observation is included in the seasonal adjustment;

- To – date of the last time series observation is included in the seasonal adjustment;

- Between – dates of the first and the last time series observations are included in the seasonal adjustment;

- Last – a specific number of observations from the end of the time series is included in the seasonal adjustment;

- First – a specific number of observations from the beginning of the time series is included in the seasonal adjustment;

- Excluding – a specific number of observations is excluded from the beginning (First) and/or end (Last) of the time series in the seasonal adjustment. With the options Last, First and Excluding the span can be computed dynamically on the series. The default setting is All.

Series span → Preliminary check

–; –

When marked, it checks the quality of the input series and excludes from a processing the highly problematic ones: e.g. these with a high number of outliers, identical observations and/or missing values above the respective threshold values. When unmarked, the thresholds are ignored and process is performed, when possible. By default, the checkbox is marked.

X11

This section includes the settings relevant for the decomposition step, performed by the X11 algorithm.

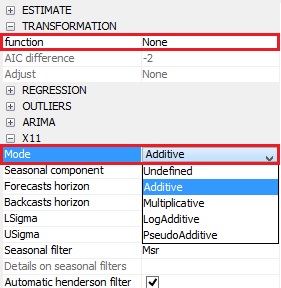

Mode

x11; mode

Time series can be regard as a composition of distinctive components: trend, seasonal component, calendar component and irregular movements. For the decomposition purpose some assumptions need to be made concerning the aggregation function that combines the components to form the linearized (stochastic) time series. The Mode parameter determines the mode of the seasonal adjustment decomposition to be performed. The choice can be made between:

- Undefined – no assumption concerning the relationship between the time series components is made.

- Additive – an original time series is decomposed into a sum of the components.

- Multiplicative – an original time series is decomposed assuming a multiplicative relationship between the components. It requires a bias correction for its trend and SA estimates1.

- LogAdditive – performs an additive decomposition of the logarithms of the series being adjusted. It requires a bias correction for its trend estimates (due to geometric means being less than arithmetic means) as well as a different calibration for an extreme value identification, which is based on the log-normal distribution2.

If Transformation is set to Log the Mode parameter should be set to Undefined (Multiplicative or LogAdditve are allowed, too). If Transformation is set to None the Mode parameter should be set to Additive. If Transformation is set to Auto, the Mode parameter is automatically set to Undefined.

The setting chosen by the user may be changed by the program automatically, if needed. The default setting is Undefined.

- PseudoAdditive – a model that assumes the following decomposition of the orginal series: $X_{t} = TC_{t} \times ( S_{t} + I_{t} -1)$, where $(TC_{t})$ is a trend-cycle, $(S_{t})$ stands for a seasonal component and $(I_{t})$ is an irregular component.

The Mode menu

Seasonal component

–; –

When the checkbox is marked, JDemetra+ computes a seasonal component. Otherwise, the seasonal component is not estimated and its values are set it to 0 (in case of an additive decomposition) or 1 (in case of an multiplicative decomposition). By default, the checkbox is marked.

Forecasts horizon

forecast; maxlead

Length of the forecasts generated by the RegARIMA model in months (positive values) or years (negative values). If Forecast horizon is set to 0, the X-11 procedure does not use any model-based forecasts but the original X-11 type forecasts for one year. The default value is -1.

Backcasts horizon

forecast; maxback

Length of the backcasts generated by the RegARIMA model in months (positive values) or years (negative values). If Backcasts horizon is set to 0 the X-11 procedure does not use any backcasts. The default value is 0.

LSigma

x11; sigmalim

Specifies the lower sigma limit used to downweight the extreme irregular values in the internal seasonal adjustment iterations. Valid values are any real numbers greater than zero with the lower sigma limit less than the upper sigma limit. The default value is 1.5.

USigma

x11; sigmalim

Specifies the upper sigma limit used to downweight the extreme irregular values in the internal seasonal adjustment iterations. Valid values are any real numbers greater than zero with the lower sigma limit less than the upper sigma limit. The default value is 2.5.

Seasonal filter

x11; seasonalma

Specifies which seasonal moving average (i.e. seasonal filter) will be used to estimate the seasonal factors for the entire series. The following filters are available:

- S3 × 1 – 3 × 1 moving average.

- S3 × 3 – 3 × 3 moving average.

- S3 × 5 – 3 × 5 moving average.

- S3 × 9 – 3 × 9 moving average.

- S3 × 15 – 3 × 15 moving average.

- Stable – a single seasonal factor for each calendar period is generated by calculating a simple average over all values for each period (taken after detrending and outlier correction).

- X11Default – 3 × 3 moving average is used to calculate the initial seasonal factors and a 3 × 5 moving average to calculate the final seasonal factors.

- Msr – automatic choice of a seasonal filter. The seasonal filters can be selected for the entire series, or for a particular month or quarter.

The default value is Msr.

Details on seasonal filters

x11; seasonalma

Period specific seasonal filters are offered as an option in X-11 in order to account for a seasonal heteroskedasticity (see description of the Cochran test under the section that describes the quality measures for X-13). This option enables the user to assign different seasonal filters to each period. It is enabled only after executing a seasonal adjustment process with settings described in the specification because only then the frequency of the series, which is necessary to define the filters, is known. For instruction how to use this parameter see the Customised seasonal filters case study. By default, this item is empty.

Automatic Henderson filter

x11; trendma

Automatic selection of the length of the Henderson filter is performed when the corresponding item is selected. Otherwise, the length given by the user in the Henderson filter item is used. By default, the checkbox is marked. The length of Automatic Henderson filter is 13.

Henderson filter

x11; trendma

Enables the user to apply the user-defined length of the Henderson filter. The option is available when the Automatic Henderson filter checkbox is unmarked. The default setting is 13 for monthly and quarterly data and 5 for half-yearly data. The length of the filters can be set to any odd number between 3 and 101.

Calendarsigma

X11; calendarsigma

Specifies if the standard errors used for the extreme values detection and adjustment are computed separately for each period (month/quarter/half-year) (All); or separately for two complementary sets of periods specified by the sigmavec parameter (Select). Other options are to compute the standard errors separately for each period only if Cochran’s hypothesis test determines that the irregular component is heteroskedastic by calendar month/quarter/half-year (Signif) or to compute them from 5 year spans of irregulars (None). The default value is None.

Sigmavec

X11; sigmavec

The parameter is displayed only if Calendarsigma is set to Select. It specifies one of the two groups of periods (months, quarters or half-years) for which a group standard error will be calculated. For each period the user sets the parameter value either to Group1 or to Group2. By default, for all periods the parameter is set to Group1.

Excludeforecasts

Xx11; appendfcst

When the checkbox is marked, forecasts and backcasts from the RegARIMA model are not used in the routine for the identification of extreme values. Otherwise, the full forecasts and backcasts are used in the extreme value process. By default, the checkbox is unmarked.

Benchmarking

The Benchmarking section allows for a benchmarking, i.e. forcing the annual sums of the seasonally adjusted data to be equal to the annual sums of the raw or calendar adjusted data.

Is enabled

–; –

Enables the user to perform a benchmarking. By default, the checkbox is unmarked.

Target

–; –

Specifies the target variable for the benchmarking procedure.

- Original – the raw time series are considered as a target data;

- Calendar Adjusted – the time series adjusted for calendar effects are considered as a target data.

The default setting is Original.

Use forecast

–; –

The forecasts of the seasonally adjusted series and of the target variable (Target) are used in the benchmarking computation so the benchmarking constraint is applied also to the forecasting period. By default, the checkbox in unmarked (forecasts are not used).

Rho

–; –

The value of the AR(1) parameter (set between 0 and 1). The default value of 1 is equivalent to the Denton benchmarking.

Lambda

–; –

A parameter that relates to the weights in the regression equation; it is typically equal to 0, 1/2 or 1. A parameter equal to 1 (default value) makes the method equivalent to the multiplicative benchmarking, while a parameter equal to 0 makes the method equivalent to the additive benchmarking.

-

When the series is logarithmically transformed, the annual mean of original series is greater than the mean of seasonally adjusted series (and of trend). It is due to the fact that the geometric mean is less than arithmetic mean. For this reason, if the bias is large the correction should be applied to avoid such discrepancies. ↩

-

GHYSELS, E., and OSBORN, D.R. (2001). ↩