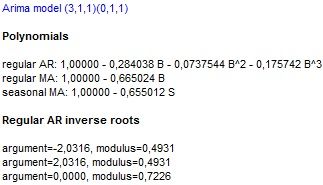

The Arima model used for forecasting

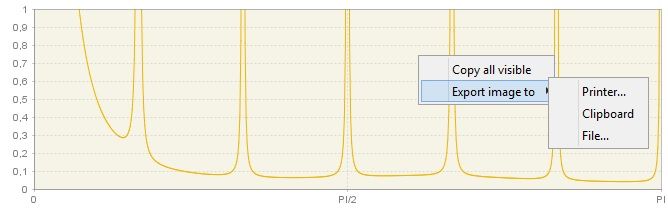

The Arima section demonstrates a theoretical spectrum of the stationary and non-stationary models. The local menu, which is available for the graph, offers the copy and export options, including sending the graph to the printer and saving the graph as clipboard or as a file in the PNG format. The Copy all visible option enables the user to export time series data to the another application.

Theoretical spectrum of the ARIMA model

In the bottom part the panel the ARIMA model used by TRAMO is presented using symbolic notation \((P,D,Q)(PB,DB,QB)\). Estimated parameters’ coefficients (regular and seasonal AR and MA) are shown in closed form (i.e. using the backshift operator1 \(B\)). For each regular AR root (i.e. the solution of the characteristic equation) the argument and modulus are given.

The details of ARIMA model used for modelling

For each regular AR root the argument and modulus are also reported (if present, i.e. if \(\mathbf{P > 0}\)) to inform to which time series component the regular roots would be assigned.

-

A backshift operator \(B\ \)is defined as: ($B^{k}x_{t} = x_{t - k})$. It is used to denote lagged series. ↩