Non-seasonal time series

The ESS Guidelines on Seasonal Adjustment (2015) recommend to apply seasonal adjustment only to those time series for which the seasonal and/or calendar effects can be properly explained, identified and estimated. Therefore, seasonal adjustment of non-seasonal time series is an inappropriate treatment. This case study explains how to recognize a non-seasonal time series using the tools and functionalities implemented in JDemetra+.

-

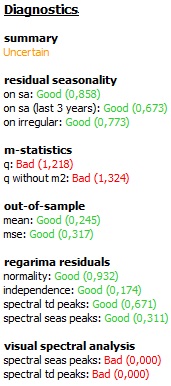

The picture below shows the results from the seasonal adjustment of a stock market turnover series from Greece using the RSA4c specification. The test diagnostics do not indicate any problems in the modelling phase (residual seasonality statistics and out-of-sample tests are displayed in green). The seasonality seems to be removed from the time series, but the overall assessment is uncertain, due to the failure of the m-statistics and the visual spectral analysis.

The diagnostic results for stock market turnover in Greece

-

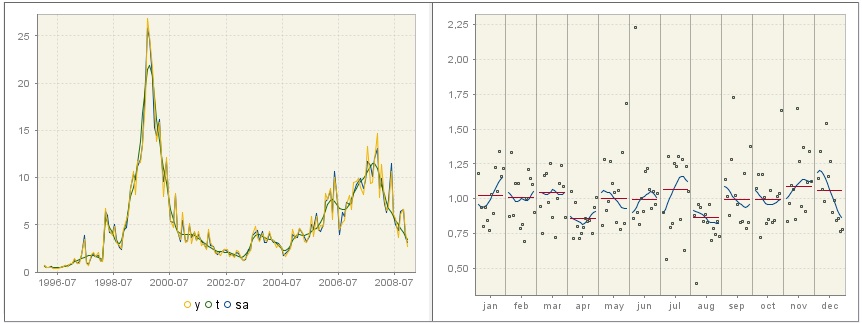

The inspection of a graph hints at the source of the problem. The original time series does not manifest any seasonal movements (left panel). It should be noted that when the X-13ARIMA-SEATS method is used for seasonal adjustment, the seasonal component is estimated regardless of the properties of the original time series (right panel). It means that the seasonal component is estimated even if there are no signs of the presence of seasonal fluctuations in the time series. In the picture below the seasonal component (blue line) is moving rather than being stable and the averages for the specific months (red lines) are not at the same level, suggesting some intra-year differences between seasons. Nevertheless, the SI ratios (dots) are rather far from the seasonal component, indicating that the irregular movements dominate over the seasonal ones.

Original and seasonally adjusted time series and the trend-cycle component (left) and SI ratios (right)

-

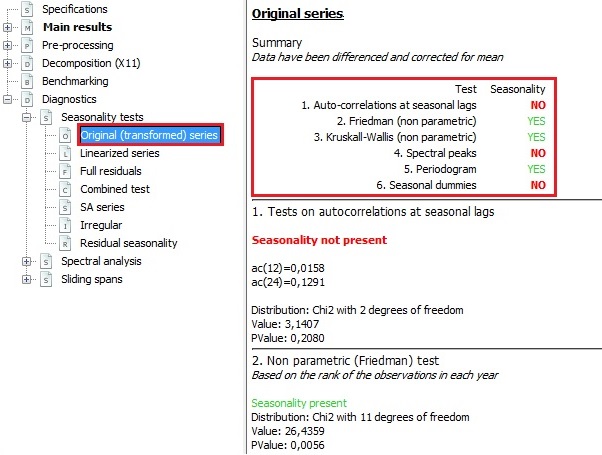

The seasonality tests performed for the original time series1 are ambiguous. Some suggest that seasonality is not present (the outcomes of three tests: the auto-correlation at seasonal lags, the spectral peaks test and the seasonal dummies test all indicate no seasonality in the original time series). These tests are available in the Diagnostic section of the output tree. The seasonality tests can be executed independently from the seasonal adjustment proces. The descriptions of these tests are given in the Seasonality tests scenario.

Seasonality test for the original (transformed) series

-

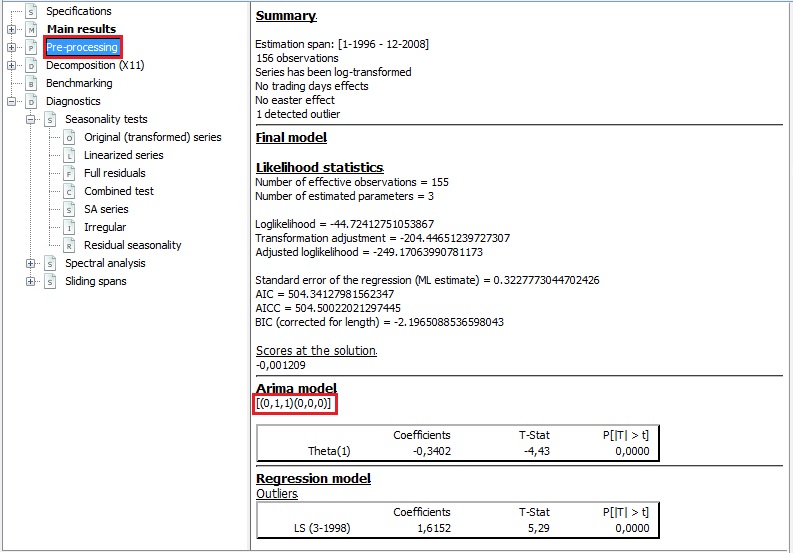

Another sign indicating that the presence of seasonality is uncertain should be addressed : the non-seasonal ARIMA model chosen by the automatic model identification procedure. The details of the RegARIMA model are available in the Pre-processing node.

Estimation results for the RegARIMA model

-

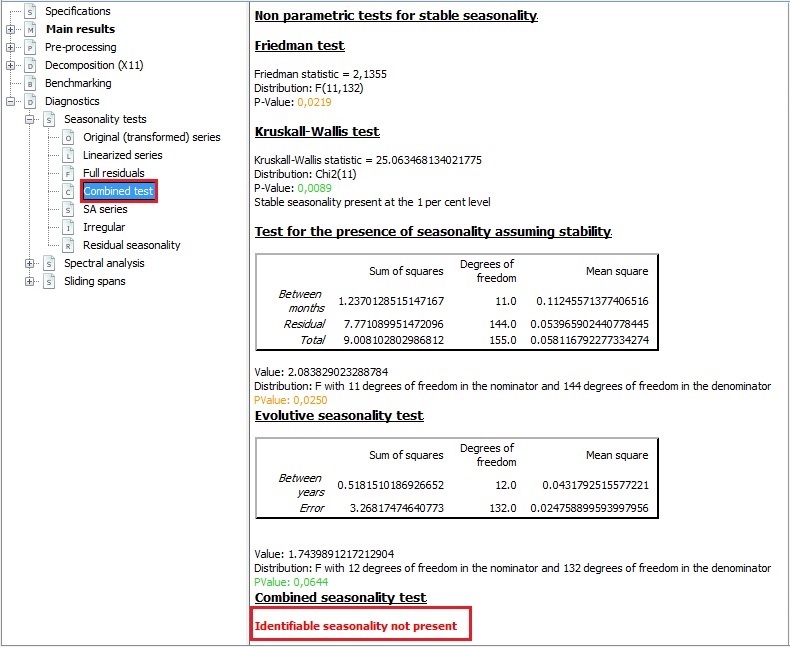

For X-13ARIMA-SEATS the most relevant tool to assess the presence of seasonal movement in the time series is a combined seasonality test. For the series presented in this case study the result of the combined seasonality test confirms that the movements observed in the time series are not stable and regular enough to be recognized as seasonal ones.

Combined seasonality test result

-

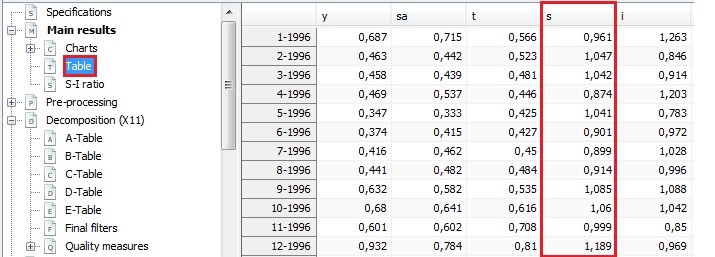

Regardless of the presence and/or significance of seasonal movements in the original time series the seasonal component is always estimated by X-13ARIMA-SEATS, as shown in the picture below (from the panel on the left choose Main results → Table). Therefore X-13ARIMA-SEATS users should always check the outcome of the combined seasonality test.

Decomposition’s results

-

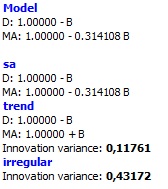

In general, in the case of a non-seasonal time series the TRAMO-SEATS method produces more coherent results than X-13ARIMA-SEATS. When no seasonal movements are detected the non-seasonal ARIMA model is used and the seasonal component is not estimated.

Decomposition result for a non-seasonal time series - TRAMO-SEATS

-

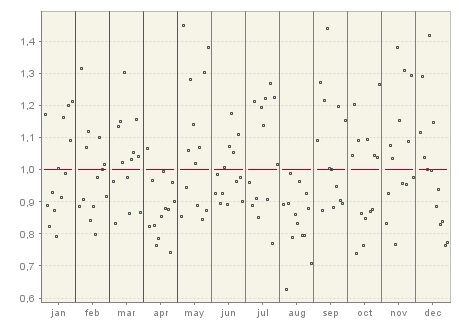

Consequently, the SI ratios (dots) estimated by TRAMO-SEATS are equal to the irregular component and for each month the seasonal component is equal to the mean (red, horizontal line), which is one.

SI ratios for a non-seasonal time series - TRAMO-SEATS

-

When the series are non-stationary differentiation is performed before the seasonality tests. ↩